Finance and nature have an interesting mathematical connection.

Legend has it that Isaac Newton’s groundbreaking work

on the laws of motion was inspired by an apple falling on his head.[1] The

story sounds apocryphal, but the great man’s contemporary biographer dutifully

recorded questions sparked by his friend’s encounter with nature. "Why

should that apple always descend perpendicularly to the ground?" Newton asked.

“Why should it not go sideways, or upwards? But constantly to the Earth’s

center?” The answers to these questions proved powerful enough to calculate to

a useful degree of accuracy the movement of everything from a small apple[2] to

the planets themselves.

There is value, then, in taking a bit of time to appreciate

nature. In fact, it can even be a great way to boost one’s net worth, as the

natural world is as much an inspiration in finance as it is in scientific

pursuits.

The ecology of

banking

That concept was put to the test not so long ago by a pair

of Englishmen inspired by the natural world. The Lord May of Oxford, an

ecologist and former Royal Society president, teamed up with Andy Haldane, the Bank

of England’s chief economist, to see if they could come up with a complex financial

model after observing the world around them.[3]

Though written a decade ago, the paper has extra relevance

today, as the authors wondered whether an understanding of the effects of a

“super spreader” contagion in nature could assist in developing public policies

that would guard against systemic flaws that spread financial contagion.

The idea wasn’t to derive a fully baked financial strategy

simply by standing outside and receiving a bit of inspiration. Rather, the

point is to see whether an analysis of natural effects offers a perspective

that’s useful in a finance, a profession where discoveries are typically made by

individuals staring at spreadsheets on computer monitors.

The

investigation took place in the wake of the 2007-2008 banking system meltdown,

and so it reflects their recent experience with that disaster. They found existing

theories failed to adequately explain the propagation of shocks and instability

within a financial system. With the interaction of the choices of millions of participants

around the world, each operating with their own sets of motivations, the

financial world is a phenomenally complex adaptive system — just like the

natural world, which consists of millions species interacting with one another.

The actions of a single investor or a single financial

institution create a ripple effects that can help or hurt multiple investors

and institutions. No investment takes place in a vacuum. In epidemiology, the

same is true. Someone infected with a disease like Covid-19 can infect friends,

family and random strangers simply by interacting with them. Most epidemics can

be traced back to a “patient zero” who spread the contagion to susceptible

individuals creating a ripple effect throughout society.

Financial shocks propagate through the banking system in a

way that’s similar to how a virus spreads. The banking system relies on a

complex series of interactions between financial institutions. For it to work,

banks must make short-term loans to one another so that everyone always has the

capital reserve needed to operate.

In this highly simplified example, a single failing bank can,

in extreme circumstances, drag down multiple institutions with which it does

business. Imagine you ask for your money back after putting $1,000 in a hypothetical

bank in which you’re the only customer. Your money isn’t put in the vault for

safekeeping. Instead, about $100 is put in reserve so the bank can use the rest

of your funds, $900, to make loans or other investments. When you come in to

reclaim your $1,000, your bank will simply borrow $900 from another bank, Bank

B, through a short-term loan.

Banks flush with cash are happy to oblige since they collect

interest for a loan that usually is paid back within 24 hours, or a week at

most. The Federal Reserve uses its power to set the reward for making such

loans as its primary tool for balancing risk levels and employment levels and

economic growth. The so-called federal funds rate has varied from 19 percent in

1981 to the meager 0.09 percent currently on offer.[4]

But what happens when a bank runs out of money after making a

series of bad loans and investments? Once the capital reserves fall below the

minimum set by the Fed, that institution is in trouble — particularly under the

rules in effect in 2007. It can’t pay back its creditors, especially Bank B.

Now Bank B is down $900, and if its assets and overnight borrowing ability are

stressed, it too will fail, further dragging down Bank B’s creditors — and so

on throughout the banking system.

The

system is more complex than this in practice, but the above is meant to provide

a basic sketch of how market liquidity shocks propagated in the 2007-2008 financial

meltdown. Consumers who had taken advantage of absurdly generous “no money

down” sorts of mortgage offerings began to default in droves. The mounting

losses crippled banks’ capacity for making interbank loans. With their reserves

run dry, banks had no money to lend to businesses and consumers. The resulting credit crunch meant businesses

couldn’t grow, and the economy stalled not just in the United States, but

worldwide.

Does nature have any advice to offer to keep history from

repeating itself, with a series of failures dragging the entire world down?

Traditionally, regulators have boosted liquidity and capital requirements to

reduce the risk of individual bank failure. May and Haldane were inspired by

ecology to address the problem holistically and came up with the idea of making

the banking network, rather than just its component parts, more resilient — a

technique used in epidemiology.

The way epidemiologists stop the outbreak of a virus spread

by interpersonal contact is to focus on the “super spreaders.” That is, efforts

go to reining in the 20 percent of individuals who are responsible for 80

percent of the spread of the disease. Typically, such outbreaks follow a

pattern in which a minority of Typhoid Marys end up having a disproportionate

ability to infect others because they have more connections with susceptible

individuals. [5]

Too-big-to-fail institutions are so large that they are the

super-spreaders of the financial world. They are much more connected to the

smaller, weaker financial institutions that regularly borrow from them to keep

their reserves topped up.

May and Haldane’s proposal was to adjust each bank’s capital

requirements “to equalize the marginal cost to the system as a whole of their

failure.” That would mean, instead of setting one-size-fits-all reserve

requirements for each bank, the rules would vary according to risk level. Bigger

banks or banks that had more connection to other banks would have to keep

greater reserves on hand.

The capital requirements would also be adjusted to rise in

boom cycles and lower during recessions to make the system more resilient to

the ups and downs of the business cycle. The net result would be a system better

able to absorb shocks without collapsing. Small institutions that don’t lend

much to others would be allowed to take more risks because the consequence of

their failure is minimal. Big banks, on the other hand, would have to take a

more conservative course because their capacity to do damage is so much higher.

Not surprisingly, Congress and international regulators have

been pushing risk-based requirements for quite some time. The Federal Deposit Insurance

Corporation (FDIC) implemented strengthened risk-based capital requirements in

2012,[6]

and the leaders of the ten largest central banks came up with proposals known

as Basel I and Basel II before that. But, as May and Haldane noted, those efforts

focused on individual institution risk rather than the systemic risk suggested

by epidemiology.

Mathematics is the

middle term between nature and finance

It’s no accident that lessons from nature can be applied to

finance, as mathematics describes the complex patterns of nature and finance alike.

Natural phenomena, from the smallest DNA molecule[7] to

the largest spiral galaxy, from flower petals to Nautilus shells, reflect a

regular pattern. One pattern that seems to appear just about everywhere was called

“mean and extreme ratio”[8] by

the ancients. They used it as a guide in building the wonders of the ancient

world like the Great Pyramid of Giza. Medieval mathematician Leonardo Bonacci,

whom we can thank for advancing the demise of Roman numerals in western

commerce and mathematics,[3]

expressed the pattern as a sequence of numbers — 1, 1, 2, 3, 5, 8, 13, 21, 34,

55, 89, 144 and so on. Each of these numbers is the sum of the preceding two

numbers.

Called the Fibonacci sequence in Bonacci’s honor, the numbers

approach what we now call the golden ratio, or 1.1618. To the extent that art

follows nature, you’ll also find the ratio in music,[9]

painting, sculpture and architecture. Da Vinci himself provided illustrations

for a book about the “divine proportion,”[10] and

artists from the Renaissance to the present day have created works that reflect

the harmony that this ratio describes in nature.

Fibonacci’s

appearance in finance

In finance, a field that doesn’t much care about aesthetics,

you’ll find some traders who use the Fibonacci numbers to make money. In 1935,

Harold M. Gartley published “Profits in the Stock Market,”[11] and on page 222 he included a set of figures describing patterns of an upward

market trend and a downward market trend. These patterns are used to this day

by traders who believe it can identify the point in which a stock price is

about to reverse — knowing that before it happens is key to turning a profit. The

idea is that when one observes the pattern on a market activity chart, it can

serve as a warning that the price is about to plunge and it’s time to sell, or,

conversely, it’s time to buy because the trend will continue sharply upward in

the case of the bullish chart.

Roughly

speaking, the “bullish” Gartley pattern resembles the letter M, while the

bearish pattern is the same figure upside-down, looking like a W. Later

analysts realized that “Gartley 222” chart described a harmonic pattern of Fibonacci

ratios. The chart starts at point X, which will either be high (in a bear

pattern) or low (in a bull pattern). The four movements that follow are

described by the letters A, B, C and D. It’s a bullish Gartley 222 when the

chart meet the following dimensions. After an upward movement from X to A, a

downward correction follows

from A to B. If AB is 61.8 percent of XA, and is followed by

a 38.2 percent rise from B to C, and then there’s a drop from C to D whose

value is 1.618 times larger than from B to C — then the chart is in play. The idea

is that it’s time to buy because the value is about to rebound.

This theory is popular enough that automated Fibonacci

sequence detection capabilities are built into trading platforms.[13] But

does it actually work? Economics professor Kuldeep Kumar and business and AI

researcher Sukanto Bhattacharya sought to find the answer.[14]

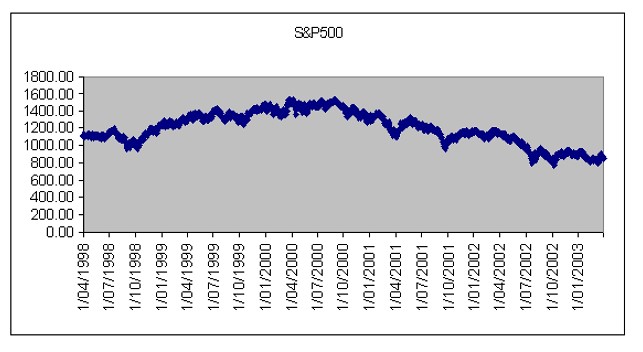

They applied computer analysis of a time-series plot of the S&P closing

values between 1998 and 2003. They noted the largest “retracements,” or

short-term changes in value, during the study period.

Right off the bat, the percentage value of the changes

approached the Fibonacci levels of 23.6 percent and 38.2 percent. The analysis

found the positive correlation between the variables was significant. While far

from conclusive, the analysis suggests there might be something to this technique.

Kumar and Bhattacharya appeared a bit surprised by their own

findings. “We are inclined to opine,” they concluded, “that all of technical

analysis is definitely not a voodoo science and there are in fact elements of

true science lurking in some of its apparently wishful formulations, just

waiting to be uncovered by the enterprising investigator.”

Scientists

are rightly skeptical of any phenomenon that defies rational explanation. But

the market is moved by the individual choices of its participants and the

automated trading scripts they author. It very well could be that the decisions

to buy and sell “feel right” at the time to

the traders seeking to balance their portfolio. Each move is

made at points that feel “natural” in the same way that an artist might frame

his subjects in a golden ratio without necessarily knowing the underlying

mathematics. Is it really that surprising that players in the market seek the

same harmony that surrounds them in nature? The more one explores the world of

biology, the more one realizes it can teach us a thing or two about finance.

Joseph Byrum is chief

data scientist at Principal. He holds a Ph.D. in quantitative genetics and his

current work is focused on developing artificial intelligence tools to provide

a measurable increase in investment accuracy.

[1]

William Stukeley, Memoirs of Sir Isaac Newton's Life (1752). MS/142, Royal

Society Library, London http://www.newtonproject.ox.ac.uk/view/texts/normalized/OTHE00001

[2]

Creative Commons photo of Newton’s apple tree, source: https://commons.wikimedia.org/wiki/File:Apple_tree_Woolsthorpe_Manor.JPG

[3]

Haldane, A., May, R. Systemic risk in banking ecosystems. Nature 469, 351–355

(2011). https://doi.org/10.1038/nature09659

[4]

https://fred.stlouisfed.org/series/IRSTCI01USM156N

[5]

Stein, Richard A. “Super-spreaders in infectious diseases.” International

journal of infectious diseases : IJID : official publication of the

International Society for Infectious Diseases vol. 15,8 (2011): e510-3. doi:10.1016/j.ijid.2010.06.020 https://www.ncbi.nlm.nih.gov/pmc/articles/PMC7110524/

[6]

https://www.fdic.gov/news/financial-institution-letters/2012/fil12026.html

[7]

Yamagishi, M.E.B., Shimabukuro, A.I. Nucleotide Frequencies in Human Genome and

Fibonacci Numbers. Bull. Math. Biol. 70, 643–653 (2008). https://doi.org/10.1007/s11538-007-9261-6

[10]

May, Mike. "Did Mozart use the golden section?" American Scientist

84, no. 2 (1996): 118+

[14] Sukanto

Bhattacharya and Kuldeep Kumar. (2006) “A computational exploration of the

efficacy of Fibonacci Sequences in Technical analysis and trading” http://epublications.bond.edu.au/business_pubs/32

{kind=link}